Under The Bonnet #1: Risk Profiling Tool

April 1, 2022

Risk profiling is a process for finding the optimal level of investment risk for clients by balancing their risk required, risk capacity and their risk tolerance. Someone’s risk required is the risk associated with the return they require to achieve their objectives given the financial resources available. Their risk tolerance is the level of financial risk they are emotionally comfortable with, and their risk capacity is the level of risk they can afford to take.

Here at Counterpoint, I use the Finametrica Risk Tolerance Profiling tool, and have been for over 10 years. While there are many risk profiling tools available, I find Finametrica to be a relative simple but thorough way to discuss the implications of risk with clients.

The tool was launched in 1998. It was developed and trialled in Australia over four years with the assistance of the University of New South Wales. It’s now maintained with expertise from the London School of Economics, and has gained international recognition as world’s best practice. The profile’s reliability and validity is backed by over a million uses by thousands of financial advisors in over 20 countries

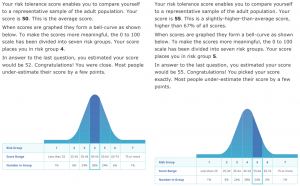

The Finametrica questionnaire consists of 25 multiple choice questions, the outcome being a risk tolerance score out of 100. This score enables us to compare their position with a representative sample of the population and put them into a risk group, following which a discussion is had to finalise the risk profile they will be assigned (e.g. balanced, growth).

Some of the current questions are:

- Investments can go up or down in value and experts often say you should be prepared to weather a downturn. By how much could the total value of all your investments go down before you would begin to feel uncomfortable?

- You are considering placing one-quarter of your investment funds into a single investment. This investment is expected to earn about twice the term deposit rate. However, unlike a term deposit, this investment is not protected against loss of the money invested. How low would the chance of a loss have to be for you to make the investment?

- With some types of investment, such as cash and term deposits, the value of the investment is fixed. However inflation will cause the purchasing power of this value to decrease. With other types of investment, such as shares and property, the value is not fixed. It will vary. In the short term it may even fall below the purchase price. However, over the long term, the value of the shares and property should certainly increase by more than the rate of inflation. With this in mind, which is more important to you – that the value of your investments does not fall or that it retains its purchasing power?

- Think of the average rate of return you would expect to earn on an investment portfolio over the next ten years. How does this compare with what you think you would earn if you invested the money in term deposits?

In addition to providing a structured approach to assigning a risk profiles to clients, it is also a great way to start broader conversations about such things as comfort with having debts, planning to maximise social security entitlements, and investments return expectations versus what is more realistic to plan based upon.

As clients’ situations change, so to can their attitudes towards risk, therefore every three years I get them to complete a new questionnaire.